By Elke Zeki

Financial planning is not an exact science, nor is it about getting everything right. It is about creating a plan that accounts for uncertainty and allows you to adjust quickly and easily.

One such area of uncertainly, especially when planning for retirement, is expected returns. When doing a cash flow analysis, we always assume a return for each asset class in your portfolio. These expected returns are usually based on very long-term averages with model adjustments resulting in minor changes.

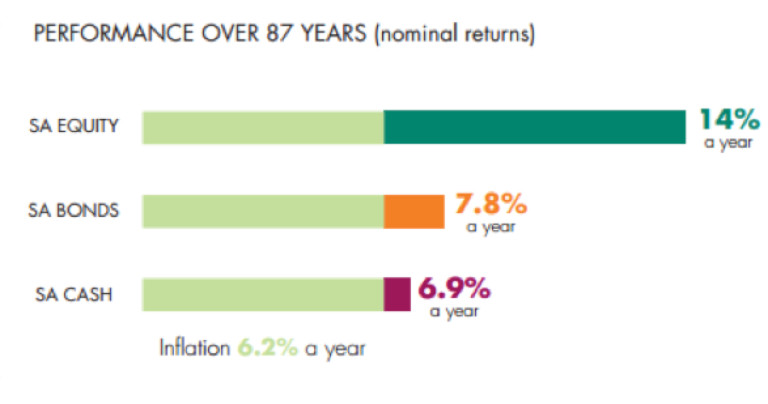

The problem with assuming average returns for equities of 14%, is that these returns do not come in a straight line. Returns from equities (and other asset classes) can be extremely volatile with some years producing much higher or much lower returns than the average assumed in our calculations.

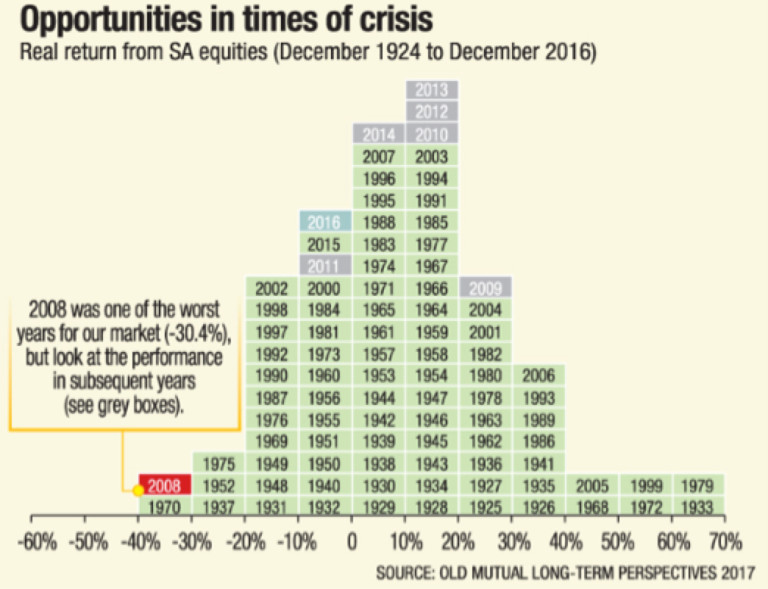

Volatility is one issue, but another is the order in which you receive these returns.

Two people with the same amount of capital, invested in the same portfolio and same monthly drawdowns, can have significantly different long-term results due to different market conditions and timing of retirement. If one retires during a strong bear market and draws income during a prolonged period of low returns, it will significantly reduce his capital and the portfolio may take years to recover from it.

We can illustrate this below by looking at another example:

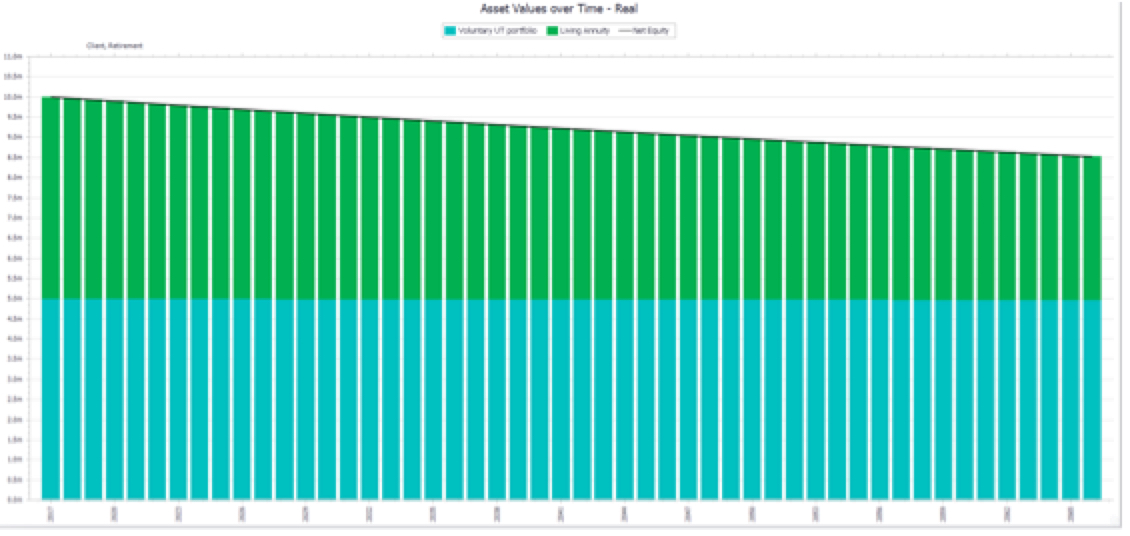

Celeste retires today

Investment summary

| Living annuity | R 5 000 000 | 5% annual drawdown (about R20 000 pm before tax) |

| Voluntary investment (Unit trust portfolio) | R5 000 000 | R20 000pm drawdown |

- She receives a total of R40 000pm (before tax)

- Income adjusted for inflation over time

- Portfolios invested to target a return of inflation + 6% based on long-term projections.

- A basic cash flow analysis would show Celeste that she could comfortably draw R40 000pm (adjusted for inflation each year) from her investments for the rest of her lifetime. The capital would be enough.

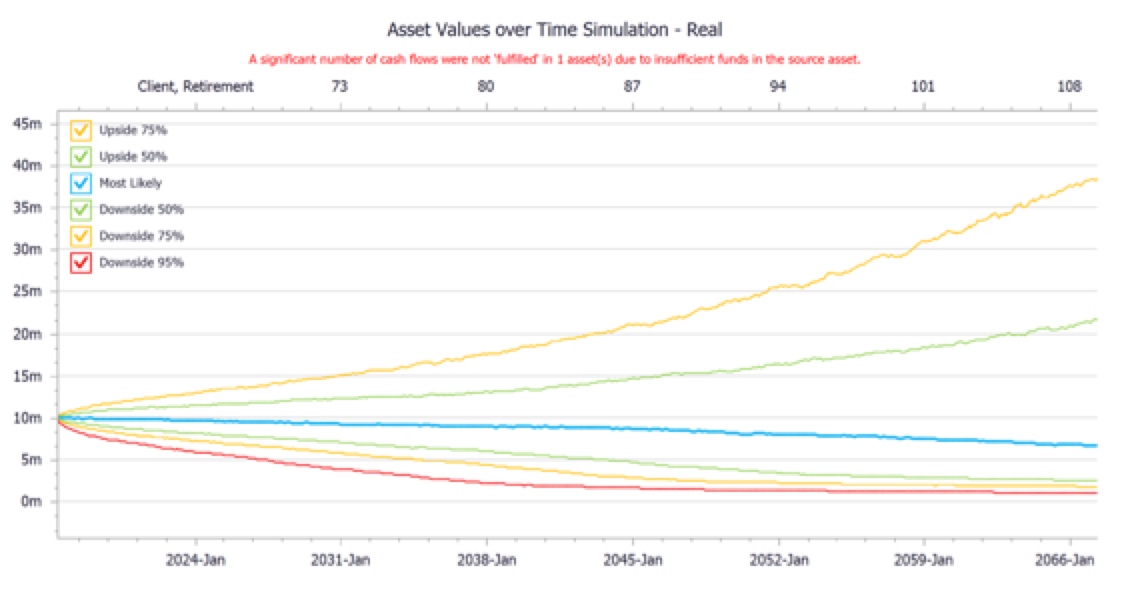

It’s possible to do a more complex analysis by simulating returns (based on actual returns received in the past). It’s a technique called Monte Carlo simulation (For more reading on the topic: http://www.investopedia.com/terms/m/montecarlosimulation.asp)

The system creates different scenarios by using historical data and randomly allocating returns to each year. Each scenario would allocate the returns in a different order thus giving us different results.

When looking at Celeste’s analysis the blue line in the graph above represents the average expected outcome into retirement. The graph also illustrates that given a certain order of returns Celeste may be worse off than planned (red line) or she could be much better off (top yellow or green lines).

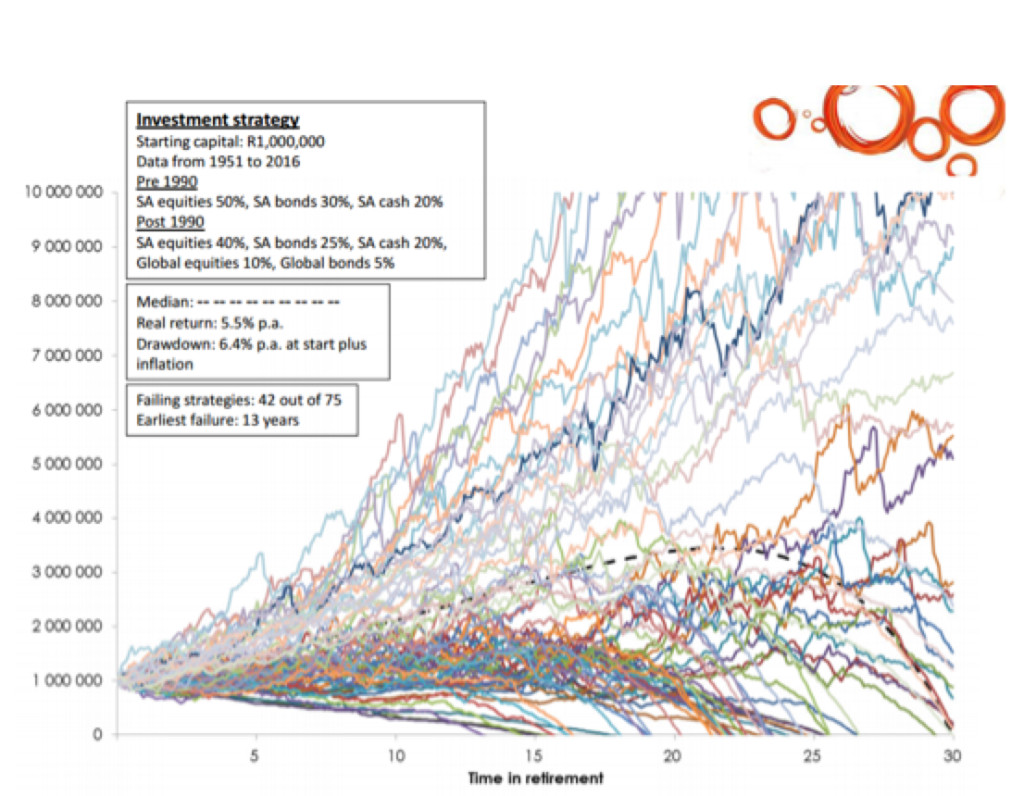

Another way of illustating this is by showing all the possible outcomes as in the example below. The black dotted line representing the average and most likely outcome.

The dispersion between different scenarios can be huge and therefore can have a significant effect on your capital and ability to retire comfortably. This is something often neglected by retirees and advisors. Most people only plan for the blue line. However as illustrated, returns are random and can present themselves in different ways

Common mistakes made to counter this problem

Reduce risk of the investments (include less volatile assets such as cash and bonds) – the problem with this approach is that if you are too conservative, your income withdrawals cannot keep up with inflation and you would therefore reduce capital quickly over the long-term.

Increase the risk of the investments (include more high growth assets such equity and property) – because equities have a higher expected long-term return than other asset classes, it can make the outcomes look more attractive. The randomness of returns and higher volatility may however increase the probability of being worse off than planned.

Only live off the income from investments – this is not always possible to do, especially if yields are low. Many people need to live off income and capital. It’s just a case of planning properly to ensure that the capital lasts your lifetime.

How to protect yourself against the risk of being worse off than planned

In our view, there are only two ways to effectively reduce your risks of reducing capital significantly. These are:

Increase diversification – good asset allocation and diversification amongst various asset classes is critical. It’s important to construct a portfolio to target a specific return by taking the least amount of risk possible. Diversification reduces risk.

Your spending/withdrawals – this is the most important and effective way to protect capital, especially in low-return years. It’s important to be conservative with your drawdowns especially in good years. Returns in good years should be banked for bad years.

How can a financial planner help?

It’s important to remember that cash flow analysis is just a guideline to provide you with some idea of what is possible. It is however something that should be monitored carefully over time, so that you can react and adjust where necessary in times of low returns.

At Foundation Family Wealth, we plan regular reviews with our clients. In our regular reviews with our retirees, we discuss with them the progress of their portfolios relative to the initial plan. At every review, we perform a new cash flow analysis based on the current value of the portfolio.

We also review the most recent experience and discuss the necessary expectation adjustments or withdrawal adjustments. We work as a team to protect our clients’ portfolios in good and bad times. Research has shown that this approach of on-going monitoring and adjustment can prevent clients from experiencing the worse case scenarios.