A prolonged, low-growth environment and no real returns from our market were the main talking points as we entered 2017. With constant negative press on corruption and a deteriorating political landscape, one can understand the inclination to be pessimistic.

Up to the midway point the pessimists were right. The stock market surprised us with a 7% uptick (locally) in July that started the rally that brings the total year-to-date return to 20%.

It was a Naspers story

Although it is not all that it seems: Naspers rose 75% in 2017 and dominates the JSE All Share Index in size, now more than 20% of that index. Without Naspers, index returns would have been more pedestrian.

The table below illustrates the returns excluding Naspers.

| Ending Oct-2017 | 1 Year | 3 Year |

| ALSI | 20.1% | 29.5% |

| SWIX | 17.3% | 28.2% |

| Naspers | 52.8% | 152.9% |

| ALSI ex Naspers | 14.2% | 18.6% |

| SWIX ex Naspers | 9.3% | 13.2% |

Below are some important points on Naspers:

- Naspers owns a 33% stake in Tencent, a Chinese investment firm that focuses on internet value add services. Tencent is listed and at the time of writing this article, the value of the stake is worth R2, 199 billion.

- At the current share price Naspers is valued at R1, 670 billion. This means markets are discounting roughly R400 billion of Tencent’s value or discounting Naspers’s other assets.

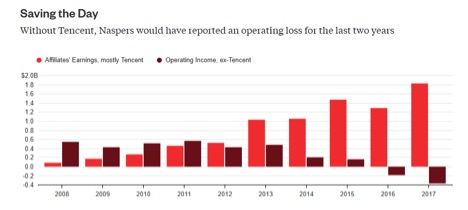

- If we strip out Tencent, Naspers has had a negative operating cash flow for the last two years of reporting, as illustrated below.

On a look-through basis, this would mean that the JSE All Share Index has more than 20% exposure to operations in Chinese tech firms. This serves as a good hedge against low growth and a weakening Rand. However, this is also a significant risk in a passive solution where flexibility is limited.

The article below gives great insight into Naspers.

Would You Bet Your Life Savings On A Chinese Internet Company?

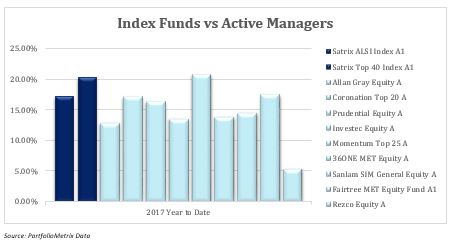

Passive or index tracking products have benefited from the rise of Naspers – passive or index products have outperformed recently. Most active managers are not allowed to hold such large positions in one share. From a risk perspective, they should have lower exposures in any event. The graph below compares 9 of the best known active equity funds to two passive index funds tracking the JSE Top 40 Index and the JSE All Share Index. Only one fund managed to outperform the Top 40 during 2017. Only 3 funds outperformed the All Share Index.

Should the Tencent story start to disappoint, there is significant risk in the Naspers share price and hence the local equity indices. Expectations from Tencent are high – it’s not hard to imagine that it could disappoint. When Naspers falters, active managers will outperform size-based indices because of their obligatory underweight positions.

It didn’t pay to ‘wait and see’

Many investors have adopted a ‘wait and see’ attitude. It is clear from the flows in and out of unit trusts – flows into money market funds or safe haven funds have increased. This has proven to be the wrong move. Markets did unexpectedly well – even active managers with well diversified portfolios delivered above average performance. This shows again that there is a low correlation between politics and short-term market returns. Investors are losing out.

Poor economic conditions do not equate to poor future market returns

The South African market is well diversified with growth predominantly coming from outside our borders. Poor local economic and political conditions do not necessarily equal poor market conditions.

In addition, the local market already discounts the continuation of poor economic conditions. Listed companies also have significant cash reserves in the current environment. A good outcome in December at the ANC Conference could lead to an uptick in business confidence with a well-needed cash injection into our domestic market. The potential is also there for an uptick in SA Inc. (all the shares with predominantly local earnings). The Financial index is up only 7% in 2017. Financial stocks are directly impacted by credit rating downgrades and currency weakness. The index is trading at a Price to Earnings ratio of 14 which is considered cheap. Active managers will be able to adjust portfolios to respond to certain opportunities should SA Inc. head into a more positive direction.

Considering almost three years of below expected returns prior to July 2017, I leave you with the following quote: “The stock market is a device of transferring money from the impatient to the patient,” Warren Buffett.