Over the years we’ve often come across the same issues affecting retirement when dealing with new clients. These common mistakes are not always obvious. Unless you run the numbers and do proper cash flow analysis, it’s not easy to see how your choices will impact your retirement.

We hope that these practical examples of what we often encounter, help you.

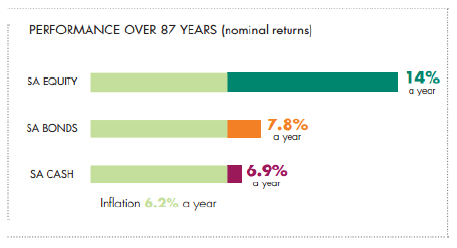

Investing funds too conservatively

This is probably the most common mistake we come across. Many people believe that investments should be made more conservatively as they approach retirement. In other words, invest the funds into low risk assets such as cash and bonds. Some people start de-risking their investments as early as age 50.

In South Africa the long-term average annual inflation rate is roughly 6%. Many argue that this inflation rate is higher for retirees due to high health care and assisted living costs. Your retirement funds therefore need to provide a return of more than 6% per annum PLUS what you withdraw annually for living expenses in order for your capital to remain intact.

Cash and bonds alone cannot do this. Drawdowns, inflation and any other unforeseen expenses will quickly deplete capital. It’s therefore important to have decent exposure to growth assets such as equity and property in your retirement portfolio. Additional asset classes also help improve overall diversification and the stability of the portfolio.

Source: Old Mutual

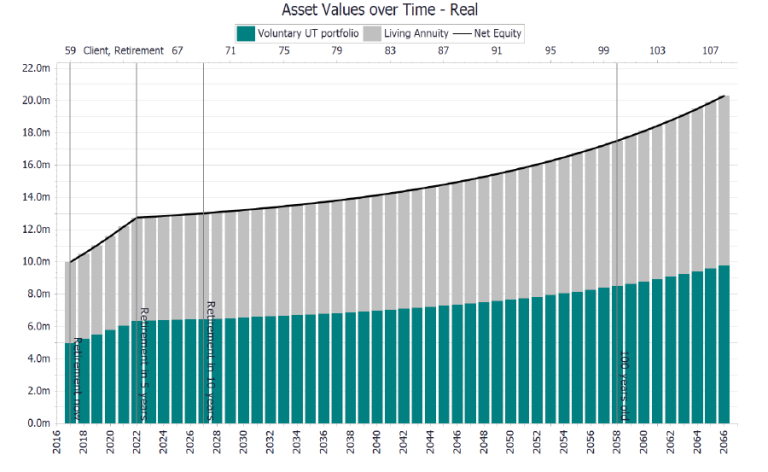

Retiring too early

One of the most powerful tools to increase the longevity of your capital in retirement is to delay withdrawals for a few years.

Take Anne for example: this graph shows the impact withdrawals (R50 000 per month) will have on this Anne’s capital if she retires at age 59.

If Anne delays retirement and starts drawing the exact same income (adjusted for inflation) 5 years later – you can see the impact on the capital is significant. In fact, the impact is so significant that Anne will not deplete capital at all.

Of course this is not always in your control. Today the pre-retirement generation (55-65) is still healthy, active and generally would prefer to work for longer. Unfortunately, many corporates in South Africa still force retirement at a certain age (usually between the age of 60 and 65). If you are however able to be more flexible or find some part time work or consulting for a few years, it’s worth considering.

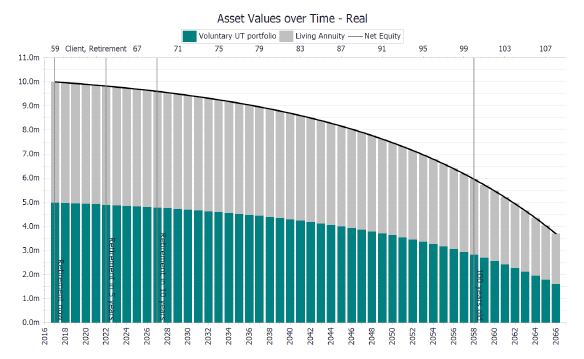

Drawing too much too early

Like retiring too early, drawing down too early can have a significant impact on the longevity of your capital. This is especially true in market cycles where returns are low or below long-term averages. Over the years we have found that people who are conservative early on, protect their capital for longer and can easily adjust income later in life when those unforeseen expenses creep up.

We use the same example of Anne. This graph shows the impact withdrawals (R50 000 per month) will have on Anne’s capital if she retires at age 59.

If Anne reduces monthly withdrawals by R5 000 pm (to R45 000pm) – the longevity of the capital is significantly increased. This in turn provides more flexibility to adjust her income if necessary.

Big ticket items

To some degree this section ties up with the previous one as it’s important to keep drawdowns to a minimum early on. An interesting trend we see amongst our hard-working baby boomers is the willingness to help their children. This may be to help them start a business or buy a first property. Another trend is to buy or renovate a holiday home.

Whilst it’s wonderful to be in a position to do these things, we would like to caution you against over spending. Increasing longevity is a reality and capital needs to last much longer. Big capital outlays early can ultimately have an impact on your income. For this reason we encourage careful planning.

You have no plan in place

It takes years to plan for retirement. This plan should include a detailed budget and cash flow analysis so that you can see exactly what income your capital (life savings) can provide during retirement. This is not always an easy and straightforward calculation, as many factors need to be considered. In our view a professional financial planner is crucial. Understanding exactly what you can and can’t do, makes it much easier to plan for retirement.

The financial markets are packed with solutions and products which make it difficult to navigate alone. Clear, objective and independent guidance can add significant value, not least of which is peace of mind.

Neglecting your health

The last bit of advice is not financial advice, but we have seen how medical expenses can ruin financial planning and put families under tremendous financial pressure. It’s so important to look after your health and to ensure that you have a good comprehensive medical aid in place before you retire. We cannot stress this enough. Looking after your health will literally change your life.

At Foundation Family Wealth we understand the importance of a good framework and financial plan, but in the same breath we understand the need for flexibility and change. Through our rigorous scenario planning and guidance, we have seen many of our clients retire successfully. If you need more information on this process, look out for our Encore workshop in March 2018. The concept of retirement has changed and it’s important to look at more than just your finances when you start planning.