The third quarter of 2018 was a tough one for emerging market economies. Turkey led the way with the Lira weakening significantly. Argentina applied for a $50 billion bailout from the International Monetary Fund, and the tit-for-tat trade battle between the US and China didn’t help the cause. South Africa fell into a technical recession as economic growth contracted for the whole of 2018.

Economics & Politics: A match made in heaven?

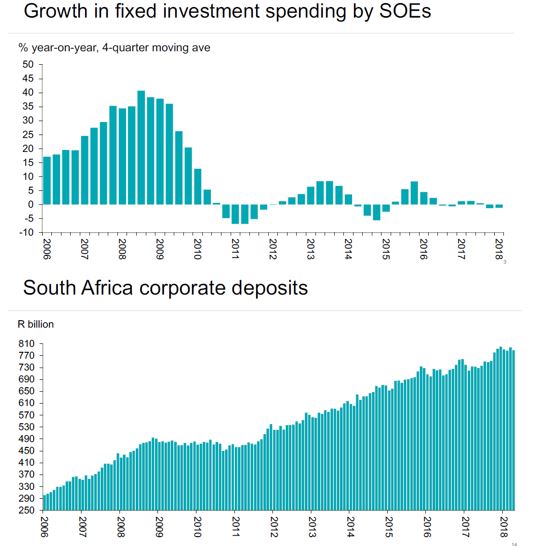

In September, President Ramaphosa announced a stimulus package to ignite growth and create jobs. Much of this had to do with restructuring government spending – however there was the announcement of an Infrastructure Fund that speaks to the two graphs above.

Over the last eight years infrastructure and fixed investment from Stated Owned Entities was non-existent. On the other side you have corporate South Africa hoarding billions of Rand’s in cash.

President Ramaphosa invited the private sector to partner with government to invest in infrastructure expansion and maintenance, which could lead to job creation and potentially be a catalyst for economic expansion. The newly appointed Infrastructure Execution Team will need to ensure projects are finished timeously as this has been a problem with similar partnerships in the past.

Smaller changes such as changing visa requirements for minors and certain countries could also lead to a boost in the tourism sector. The inflow of investments could lead to job creation on various fronts, which we drastically need.

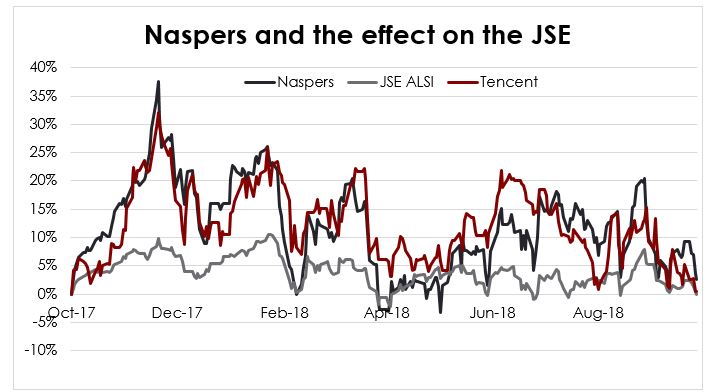

Naspers falls from grace

Naspers is the biggest company on the JSE making up more than 18% of the All Share index. Naspers’s major holding is a Chinese tech stock – the biggest social media and games publisher in China called Tencent. Tencent was rocked by a sell-off in tech stocks globally, but more importantly, the Chinese government has not issued a gaming license since March of this year. This creates uncertainty on the future potential for growth and the share price has tumbled since.

Given the size of Naspers in the All Share Index – this has serious ramifications for our local markets (as can be seen by the swings in the grey line above). At the time of writing this article, Naspers is down 11% for the year up to the end of September and down 21% for the year. Active fund managers are unlikely or even limited by regulation to assign such a big weighting to one stock – but it’s still worth noting that no company or sector is too big for a correction.

Technical Recession: What Now?

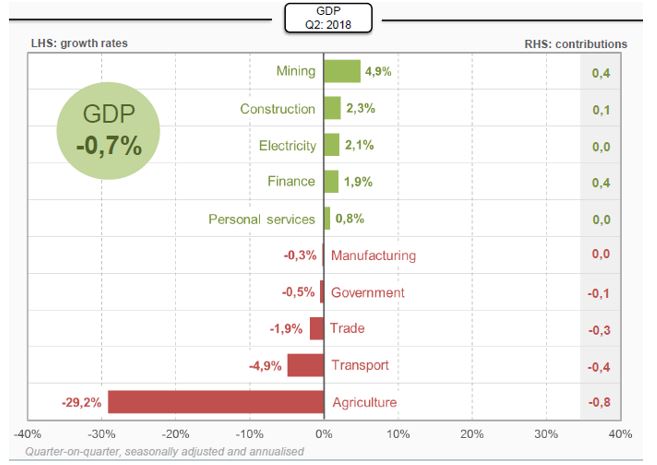

In September, South African Gross Domestic Product (GDP) growth was in the red for a second consecutive quarter, which means that we are now in a technical recession for the first time since the financial crisis in 2009. With unemployment over 25% since 2016 and business confidence at very low levels, this comes as no surprise.

Agriculture was the main detractor down 29% from the previous quarter. Mining made a healthy contribution towards growth as commodity prices recovered. But what do we do to get out of this? The investor conference at the end of the month could provide some answers. The conference is part of President Ramaphosa’s drive to get $100 billion in new investment into our country. Some analysts predict that we might exit the recession as soon as the third quarter, which would mean that we see growth above 0%. The growth targets have been revised from 1.5% to 0.6% for the year so analysts are not expecting a massive turnaround.

Turkey: Is South Africa next?

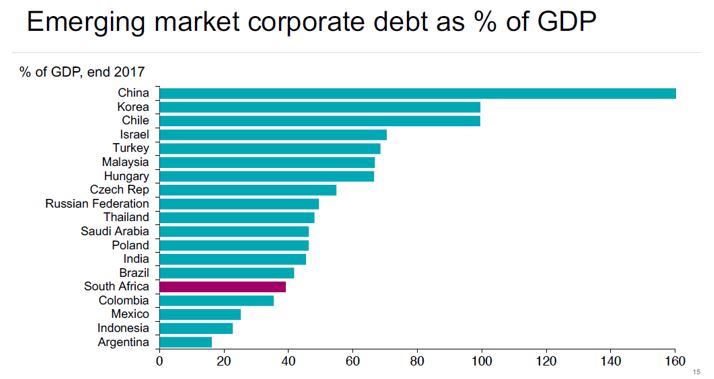

Contrary to South Africa, Turkey reported second quarter GDP growth north of 7% in 2018. This was, however fueled by foreign-currency debt racked up by the corporate sector. As the economy was overheating, inflation jumped above the central bank’s target all the way to 16%. President Erdogan did not allow the central bank to raise interest rates to combat inflation. This led to the Lira weakening by 40% which means the foreign debt got a lot more expensive in a matter of weeks.

The single biggest difference between South Africa and Turkey is our corporate debt levels compared to GDP. As per the graph, SA Corporate Debt to GDP sits just under 40% where Turkey’s is well over 50%. Secondly, we still have an independent Reserve Bank that has managed to keep inflation well within the inflation band of 3-6% and has the flexibility to hike interest rates when needed.

Even though Turkeys situation has negatively affected the Rand and all emerging market economies, it is highly unlikely that we will see a similar situation locally. The situation in Turkey brings with it uncertainty which in turn contributed to the selloff that we have seen in recent months.

In Summary

Locally, resources led the way over the quarter, continuing its stellar performance up 21% in 2018. However, equities in total declined by nearly 4% over the quarter. Cash was the best performing asset class (+ 1.7%) for the quarter. The Rand lost ground to the dollar due to the emerging market selloff. The US also raised their interest rates for the third time this year and suggested a possible four hikes to come, which could lead to further dollar strength.

Global equities had a good quarter, ending up 4.3%. America led the way with the S&P 500 up more than 7% this quarter bringing the total return to 10% in 2018. Japan’s Nikkei index reached a 27-year high on renewed optimism for earnings growth and a weaker Yen.

With global markets running hot, emerging markets out of favour and South Africa still sorting out its own house – it may seem hopeless. We have rarely seen a more pessimistic environment. The reality is that we’re all hoping for a quick fix to an eight-year mistake. This process of dismantling the Zuma-era-damage will take longer than anticipated, but if we look closer we are certainly on a better path compared to a year ago. Furthermore, Rand weakness is not necessarily bad for investor returns – a large portion of the local market is exposed to global currencies. Goldman Sachs called South Africa “the big emerging market story of 2018”. They may have been out by a year.

There is not much correlation between current economic conditions and future investment returns. At times of pessimism, remaining calm and invested in growth assets, is key. In the wake of this, we leave you with a final quote by Benjamin Graham, also known as the father of value investing: “The intelligent investor is a realist who sells to optimists and buys from pessimists.”

<Foundation Family Wealth is an Authorised Financial Services Provider>