Retrenchment is an unfortunate event that can cause a lot of uncertainty and anxiety. With it come many financial and retirement implications. This section offers some guidelines to help you navigate some of the decisions you or someone else may need to make.

What happens to my pension fund?

If you belong to a company pension or provident fund, the rules of that fund will determine your access to your retirement capital on resignation or retrenchment.

The rules of thumb for a pension fund are:

- It can be transferred in full to a preservation fund (at any service provider of your choice). There is no tax consequence for this.

- You can take a partial withdrawal from the fund (taxable), and the balance will the transferred to a preservation fund (at any service provider of your choice).

- You can decide to transfer the pension fund to your new employer’s pension fund.

The rules of thumb for a provident fund are:

- It can be transferred in full to a preservation fund (at any service provider of your choice). There is no tax consequence for this.

- You can take a full or partial withdrawal from the fund (taxable), and the balance will the transferred to a preservation fund (at any service provider of your choice).

Preservation funds are vehicles used to preserve the capital that you have already saved towards your retirement.

The cons:

You are not able to make further contributions.

The pros:

You may make one withdrawal from the fund before retirement, and this can be up to 100% of the value of the fund. This withdrawal is taxable but does allow you access to capital if necessary.

But a word of caution here: if you withdraw some (or all) of your retirement savings you will have to replace it with future savings, and often, this is very difficult to do. Still, if times are really tough and there isn’t another option for financial survival, then a preservation fund will allow temporary relief until you are able to make another plan.

Retrenchment packages and tax issues

If you are in the unfortunate situation of being retrenched, it’s important to acknowledge and understand that there are tax consequences to your retrenchment benefits.

If you have been with your employer for at least one year, you are entitled to one week’s salary for every completed year of service. This is called severance pay, or more commonly a “retrenchment package”.

At retrenchment, there are usually one or more of the following components that become payable as a lump sum:

- Salary for notice period.

- Accumulated leave.

- Pro-rata bonus/incentives.

- Retrenchment lump sum (or “severance pay”).

The first three components are taxed according to your marginal tax rate, in other words, it will be reflected on your final payslip and income tax will be deducted.

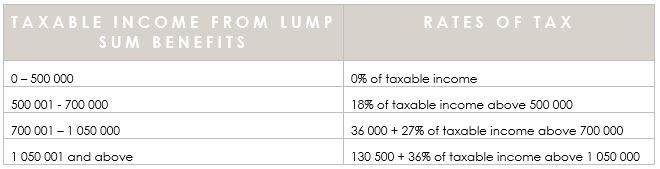

The severance pay-component is taxed according to the same table that would have applied at normal retirement. This table applies regardless of your age: if you are retrenched at 35 you will pay the same rate of tax of someone who is retrenched at 55.

This all looks great in principal: if I receive R600 000, the first R500 000 is tax free and I only have to pay tax on the remaining R100 000. Fantastic!

Or is it?

To better answer that question we have to rewind and take it one step back. One of the advantages of saving monthly into a retirement annuity or pension fund (or if you already have previous funds saved in a preservation fund), is the ability to withdraw a 1/3rd of the value in cash at retirement. The balance is then transferred to a life/living annuity that will pay a monthly income during retirement years – or however long the capital lasts.

As tax payers we are all allowed to take a full 1/3rd of the value of the fund cash, and if you have more than one retirement savings product you may take a 1/3rd cash withdrawal on each. The caveat is that you will receive a maximum of R500 000 tax free – this is across all your different retirement savings vehicles and it includes any previous retrenchment lump sums.

Let’s take an example:

Mr. Moneybags retires at age 60 with a retirement annuity worth R6m. He is able to withdraw a 1/3rd (R2m) as a cash lump sum. We already know that only the first R500k is tax free, and he then has to pay tax on the R1.5m (total tax of R472 500).

However, if Mr. Moneybags had a retirement annuity of R6m and a pension fund of R4.5m the scenario is slightly different. He is now able to take a 1/3rd of the cash of each (R2m and R1.5m) but is still only able to take the first R500k tax-free, and the portion that he now has to pay tax on is R3m (total tax of R1 012 500).

To get to the crux of the retrenchment-story from a tax perspective, let’s tweak the example one more time.

Let’s now assume that Mr. Moneybags was retrenched a number of years ago, and he received a severance benefit (retrenchment lump sum amount) at that time of R500k. He now retires at age 60 with his retirement annuity and pension fund and wants to take a full 1/3rd withdrawal from each.

Because he previously utilised the R500k tax-free portion when he was retrenched, the entire cash withdrawal will be now be taxed (total tax of R1 192 500).

The point that we would like to illustrate here is that tax benefits at retrenchment directly impact the level of tax benefit at normal retirement.

If you are retrenched and receive a lump sum benefit, you do not have a choice on how the tax will be applied. You will immediately start using a portion of your R500k tax-free allowance. Thereafter you will have to make a decision at retirement about whether you want to make further cash withdrawals from your retirement savings – being cognisant of having already used your R500k tax-free allowance.

This is where the specialised advice of a Certified Financial Planner is of critical importance. Paying the tax in order to get the cash out of your retirement savings does make sense in many scenarios, but it will differ from person to person and you need to seek expert advice at this point – the conclusion will be different for each individual.

Let us know if you need help you with cash flow analysis, scenario planning and/or tax estimates for your particular set of circumstances.